INTRODUCTION

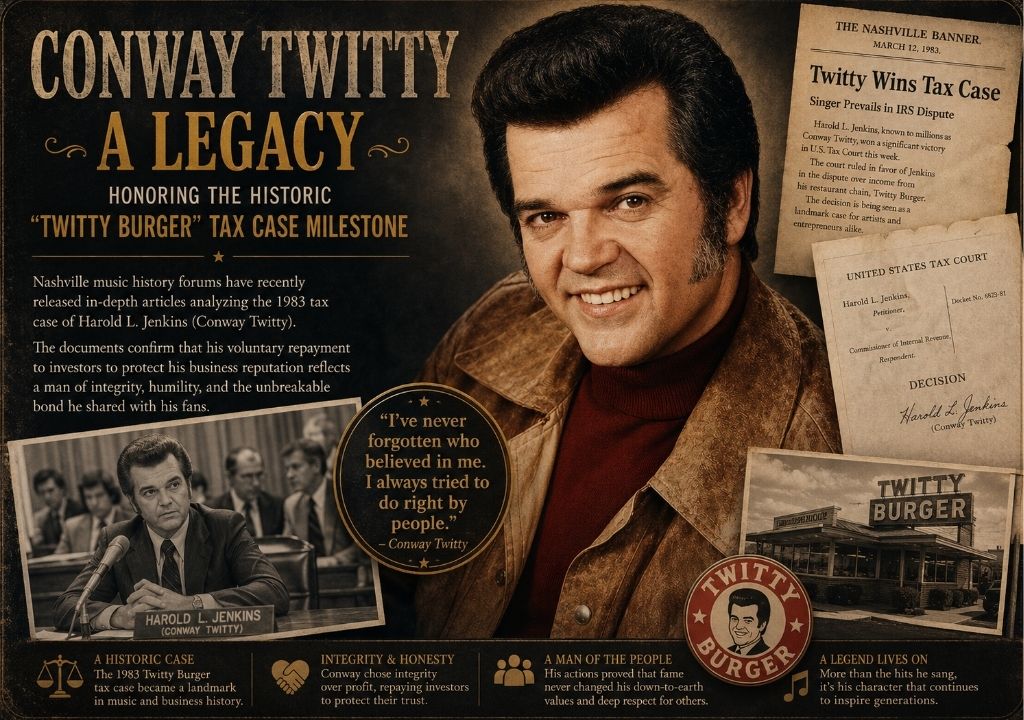

In the high-stakes financial ledger of country music, a line item from 1983 remains one of the most intellectually compelling chapters in Nashville history. When federal tax authorities challenged Harold L. Jenkins—known globally to millions of country music aficionados as Conway Twitty—they expected a standard corporate dispute over a failed fast-food venture called Twitty Burger. Instead, the ensuing legal battle, Jenkins v. Commissioner, formalized an extraordinary reality about the mechanics of fame. Nashville historical forums recently revisited this landmark case, uncovering archives that detail how Twitty bypassed legal loopholes to voluntarily repay $530,000 of his own capital to personal investors. This calculated maneuver was not merely a defensive financial strategy; it was a profound, heartfelt declaration of loyalty to the fans who anchored his multi-million-dollar empire, proving that a country icon’s most valuable asset is an unvarnished reputation of absolute trust.

THE DETAILED STORY

The structural genesis of the Twitty Burger crisis dates back to the late 1960s, when Conway Twitty sought to diversify his earnings by launching a regional fast-food chain. When the venture ultimately collapsed under severe economic pressure in 1971, standard corporate logic dictated that the limited liability structure would absorb the losses, leaving investors to bear the financial brunt. However, Twitty recognized that the currency of country music stardom operates on an entirely different moral architecture than traditional corporate America. Over the subsequent years, utilizing the substantial revenue generated from his continuous string of number-one country hits on the Billboard charts, Twitty methodically repaid every single cent to the individuals who had trusted his name, culminating in the historic US Tax Court showdown on 11/03/1983.

The legal core of the case centered on whether these repayments could be deducted as ordinary and necessary business expenses required to protect his livelihood as an entertainer. While the Internal Revenue Service aggressively argued that these outlays were non-deductible personal capital losses, Twitty’s legal counsel presented a masterful narrative concerning the absolute codependency between a country music star and his audience. To alienate investors—many of whom were prominent figures within the tight-knit country music community and devoted fans—would dismantle the foundational trust that fueled his multi-million-dollar concert ticket and record sales.

In a historic ruling that remains a masterclass in judicial literature, the Tax Court ruled overwhelmingly in Twitty’s favor. The presiding judge famously concluded that the country star’s actions were entirely essential to preserving the integrity of his business persona. This landmark victory permanently altered corporate tax interpretation within the entertainment industry, establishing a legal precedent for the tangible value of professional goodwill. More importantly, recent retrospectives across major industry trade publications like Variety and The Hollywood Reporter emphasize that the “Twitty Burger” decision codified the true nature of Twitty’s legacy. It solidified his image as an unyielding gentleman of the genre, proving that his rustic sincerity was an absolute reality rather than a calculated marketing construct.